In the world of Singaporean finance, the shift to SFRS(I) 9 represented a landmark transition toward global transparency. While the names “SFRS(I) 9” and “IFRS 9” are often used interchangeably, understanding the specific context of Singapore’s adoption is crucial for businesses operating in the Lion City.

As of 2026, Singapore remains fully committed to this framework, with recent updates further aligning it with global sustainability and debt reporting requirements.

SFRS(I) 9 vs. IFRS 9: The Core Concepts

Both standards govern Financial Instruments, replacing the older, more complex IAS 39/FRS 39 models. They focus on three main pillars:

1. Classification and Measurement

IFRS 9:

Uses a “Business Model” test and a “Contractual Cash Flow” (SPPI) test to decide if an asset is measured at Amortised Cost, Fair Value through Other Comprehensive Income (FVOCI), or Fair Value through Profit or Loss (FVTPL).

SFRS(I) 9:

Adopts these identical criteria. It ensures that a Singaporean bank’s balance sheet is readable and comparable to a bank’s in London or New York.

2. The Impairment Model (Expected Credit Loss)

The most significant change was the move from an incurred loss model to the Expected Credit Loss (ECL) model.

The Logic:

You no longer wait for a “trigger event” (like a missed payment) to recognize a loss. Instead, you must account for potential future losses from day one.

The Difference:

There is no technical difference between the two standards here. Both require a three-stage approach based on the change in credit risk since initial recognition.

3. Hedge Accounting

Both standards aim to align accounting more closely with a company’s actual risk management strategy. This makes it easier for entities to reflect their hedging activities—like currency or interest rate swaps—in their financial statements without the “artificial” volatility seen under older standards.

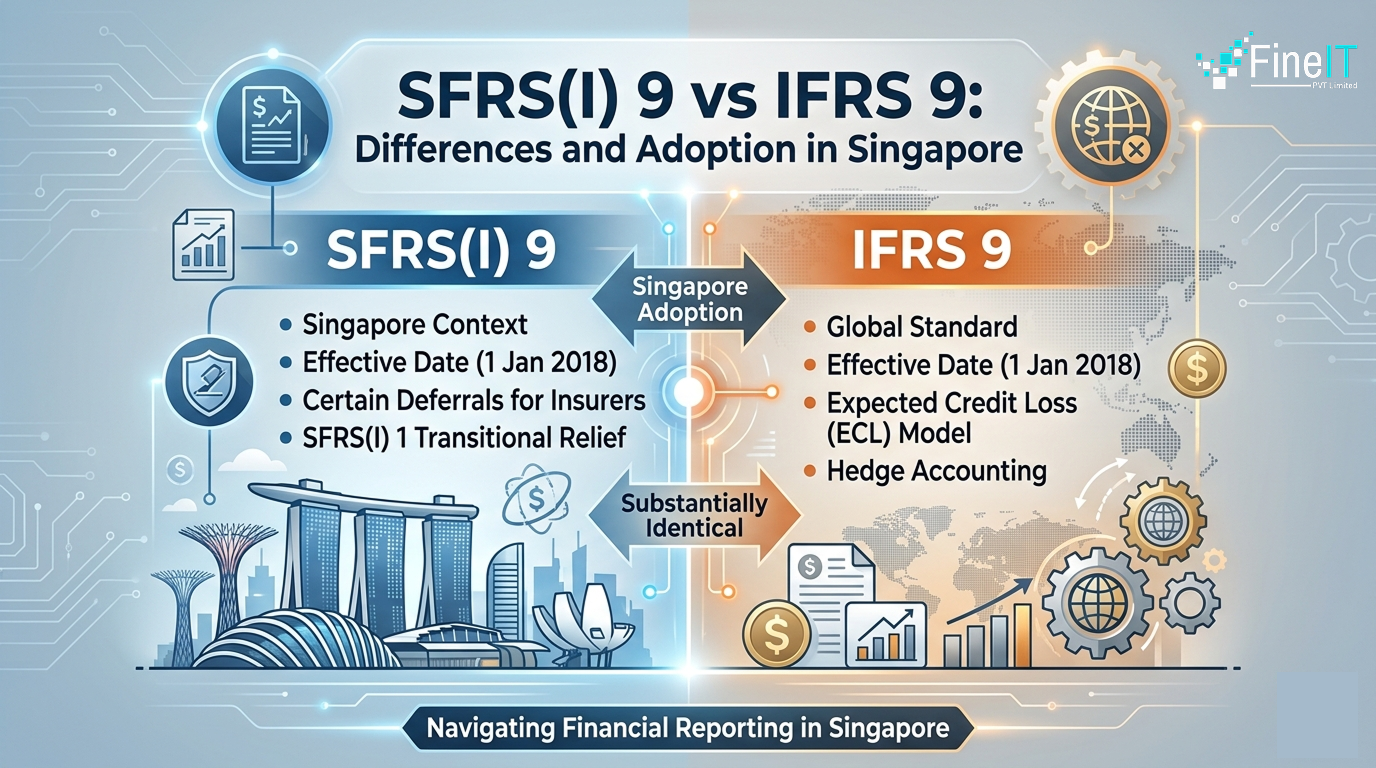

Key Differences: Is there a “Singapore Twist”?

Technically, SFRS(I) 9 is identical to IFRS 9. The “International” in parentheses—SFRS(I)—was specifically added to signal that any company complying with this standard can also claim full compliance with IFRS.

However, there are contextual differences in how they are managed:

| Feature | IFRS 9 (International) | SFRS(I) 9 (Singapore) |

| Issuer | IASB (International) | ASC (Singapore) |

| Effective Date | 1 January 2018 | 1 January 2018 (Full Adoption) |

| SME Treatment | Use “IFRS for SMEs” | Can use “SFRS for Small Entities” (which is simpler) |

| Tax Integration | Varies by country | Closely integrated with IRAS (tax) guidelines |

| Transition | Standard IFRS 1 rules | Use of SFRS(I) 1 for first-time adopters |

The “Insurance” Exception

One of the few historical differences was the deferral for insurers. Singapore allowed certain insurers to delay the adoption of SFRS(I) 9 until 2023 to coincide with the rollout of the insurance-specific standard, SFRS(I) 17. By 2026, this gap has closed, and the two are now in full synchronization.

The Adoption Landscape in Singapore

1. Listed Companies vs. Private Entities

Since 2018, all Singapore-incorporated companies listed on the SGX must use the SFRS(I) framework. Private companies have the option but often choose it if they have international stakeholders or plan to go public.

2. Tax Implications (IRAS)

In Singapore, the Inland Revenue Authority (IRAS) generally aligns tax treatment with SFRS(I) 9. For example, the “FRS 109 Tax Treatment” allows companies to align their tax reporting for financial instruments on a revenue account with their accounting treatment, reducing the need for complex tax adjustments.

3. 2026 Updates: Sustainable Debt

As of 2026, new amendments to SFRS(I) 9 (mirroring IFRS 9) have been introduced to address Sustainable Debt. This includes clarifications on how to account for financial instruments with “ESG-linked” features, ensuring that green bonds and sustainability-linked loans are measured accurately without triggering unnecessary fair value volatility.

Conclusion

The “vs.” in SFRS(I) 9 vs. IFRS 9 is largely a matter of jurisdiction rather than content. For a Singaporean business, adopting SFRS(I) 9 is not just about compliance; it’s a “passport” to global capital markets.

At FineIT, we support financial institutions across Singapore with end-to-end IFRS 9 and SFRS(I) 9 implementation—from ECL modeling and risk analytics to automated regulatory reporting.

Discover how FineIT can streamline your IFRS 9 compliance.

🌐 https://fineit.io

Request a demo: https://fineit.io/request-demo

Muzammal Rahim Khan is the CEO and Co-Founder of FineIT, bringing over 15 years of expertise in software development, implementation, and technical consulting across global markets including the U.S., U.K., Europe, Africa, and Asia. He has led the design and delivery of enterprise-grade solutions that modernize compliance, risk management, and financial reporting for banks and financial institutions. Under his leadership, FineIT has built flagship platforms such as Estimator9 (IFRS 9) and ContractHive (IFRS 16), empowering clients with automation, accuracy, and audit-ready confidence. Muzammal combines deep technical knowledge with strategic vision, driving innovation that bridges regulatory requirements with practical, scalable technology. His focus remains on building resilient, future-ready solutions that strengthen trust and efficiency in financial services.