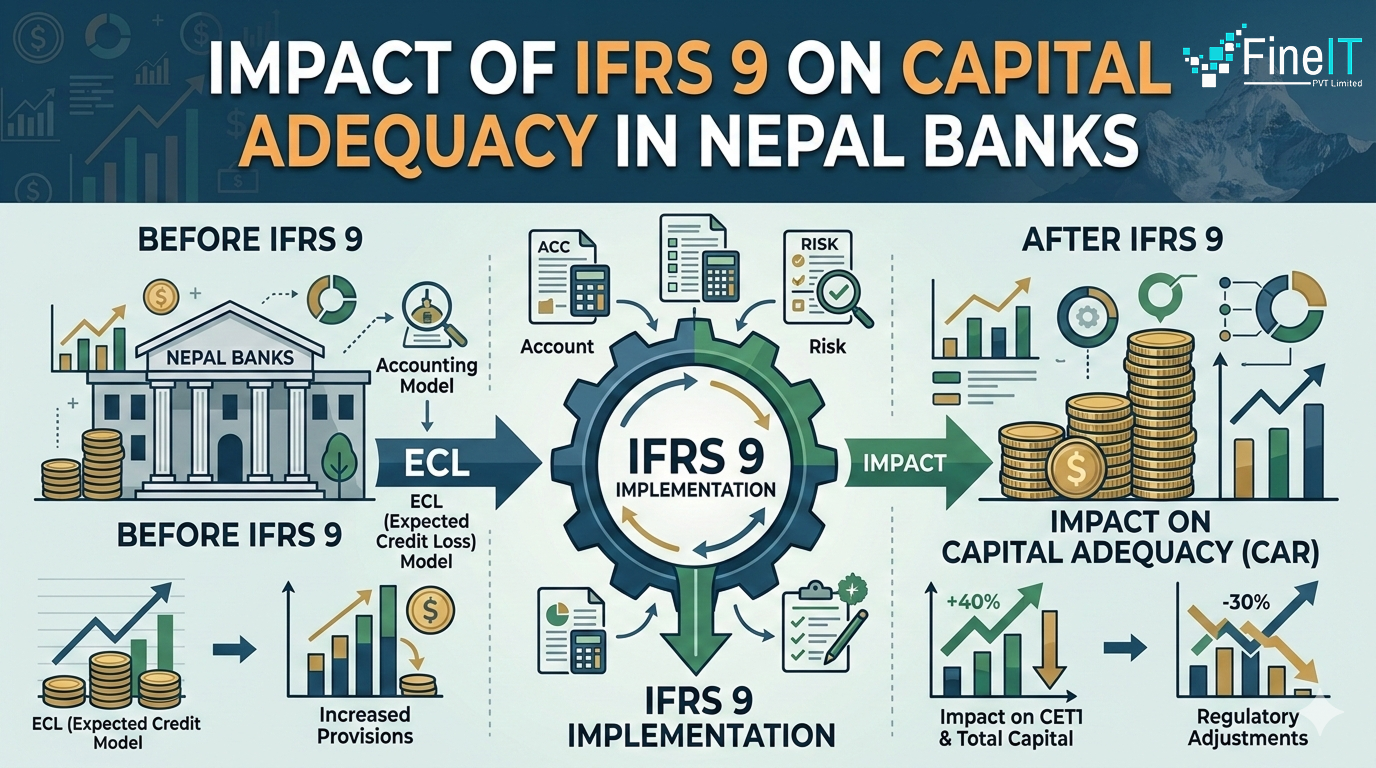

The transition from the traditional “incurred loss” model to the International Financial Reporting Standard 9 (IFRS 9)—locally implemented as NFRS 9—marks a paradigm shift for the Nepalese banking sector. As Nepal Rastra Bank (NRB) pushes for full compliance by 2025/2026, the primary concern for stakeholders is how this accounting change will squeeze the Capital Adequacy Ratio (CAR) of commercial banks.

1. The Core Shift: From Incurred to Expected

Under the old regime (NAS 39), banks in Nepal recognized losses only when a “trigger event” occurred (e.g., a payment was missed). IFRS 9 introduces the Expected Credit Loss (ECL) model, which requires banks to look into the future.

Stage 1 (Performing):

12-month ECL recognized from day one.

Stage 2 (Underperforming):

Lifetime ECL recognized if credit risk increases significantly.

Stage 3 (Non-performing):

Lifetime ECL recognized once default occurs.

2. Immediate Impact on Capital Adequacy

The move to ECL inherently leads to higher provisioning. In Nepal, where many banks have historically operated on thin capital margins, this has two direct effects on capital adequacy:

Reduction in Retained Earnings:

Higher provisions are deducted from the profit and loss account, reducing the pool of retained earnings that counts toward Tier 1 Capital.

CET1 Volatility:

As the economy fluctuates, ECL models react to forward-looking macroeconomic indicators (like GDP growth or inflation). This can cause sudden drops in the Common Equity Tier 1 (CET1) ratio during economic downturns.

3. Challenges Specific to the Nepalese Context

Implementing IFRS 9 in Nepal isn’t just a mathematical exercise; it face unique local hurdles:

Data Scarcity:

Calculating “Probability of Default” (PD) and “Loss Given Default” (LGD) requires years of historical data that many local banks haven’t systematically archived.

Macroeconomic Linkages:

Nepal’s economy is sensitive to external shocks (remittances, tourism). Integrating these volatile factors into credit models can lead to “procyclicality,” where banks are forced to hike provisions exactly when the economy is struggling, further tightening credit.

Regulatory Parallelism:

NRB often maintains “Prudential Norms” alongside IFRS. Banks may find themselves in a “double provisioning” trap where they must meet both the accounting ECL and the regulator’s minimum percentage-based reserves.

4. Strategic Response for Banks

To maintain healthy capital levels, Nepalese banks are likely to:

Rebalance Portfolios:

Shift toward low-risk assets or collateral-backed lending to minimize ECL charges.

Capital Buffers:

Issue more “Rights Shares” or “Debentures” to bolster Tier 1 and Tier 2 capital ahead of full implementation.

Tech Investment:

Deploy advanced Risk Management Systems (RMS) to ensure that credit risk is accurately priced, preventing over-provisioning.

Conclusion

While IFRS 9 initially exerts downward pressure on capital adequacy by requiring “earlier and higher” provisions, the long-term benefit is a more resilient financial system. By forcing banks to acknowledge risks before they crystalize, Nepal’s banking sector will be better equipped to handle shocks, ultimately protecting depositors and the broader economy.

FineIT provides end-to-end solutions for ECL modeling, risk management, and IFRS 9 compliance, helping financial institutions build a stronger and more resilient banking framework.

Muzammal Rahim Khan is the CEO and Co-Founder of FineIT, bringing over 15 years of expertise in software development, implementation, and technical consulting across global markets including the U.S., U.K., Europe, Africa, and Asia. He has led the design and delivery of enterprise-grade solutions that modernize compliance, risk management, and financial reporting for banks and financial institutions. Under his leadership, FineIT has built flagship platforms such as Estimator9 (IFRS 9) and ContractHive (IFRS 16), empowering clients with automation, accuracy, and audit-ready confidence. Muzammal combines deep technical knowledge with strategic vision, driving innovation that bridges regulatory requirements with practical, scalable technology. His focus remains on building resilient, future-ready solutions that strengthen trust and efficiency in financial services.