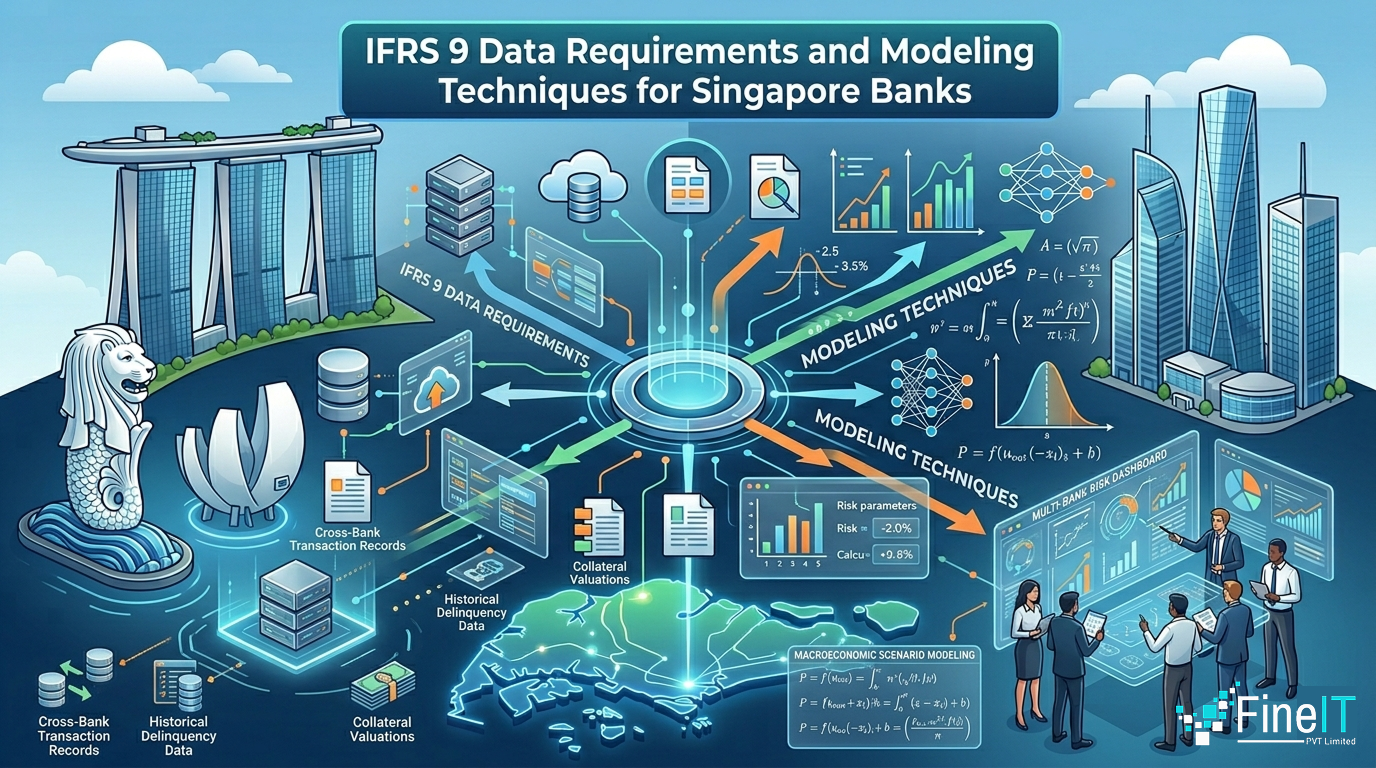

Navigating IFRS 9 in Singapore’s Banking Landscape

Navigating IFRS 9 within Singapore’s sophisticated banking sector is no longer just an accounting exercise it is a fundamental strategic requirement. Since the implementation of SFRS(I) 9 (the Singapore equivalent of IFRS 9), financial institutions have shifted from a “reactive” to a “proactive” stance in managing credit risk. For banks operating in a global hub […]