SFRS(I) 9 vs IFRS 9: Differences and Adoption in Singapore

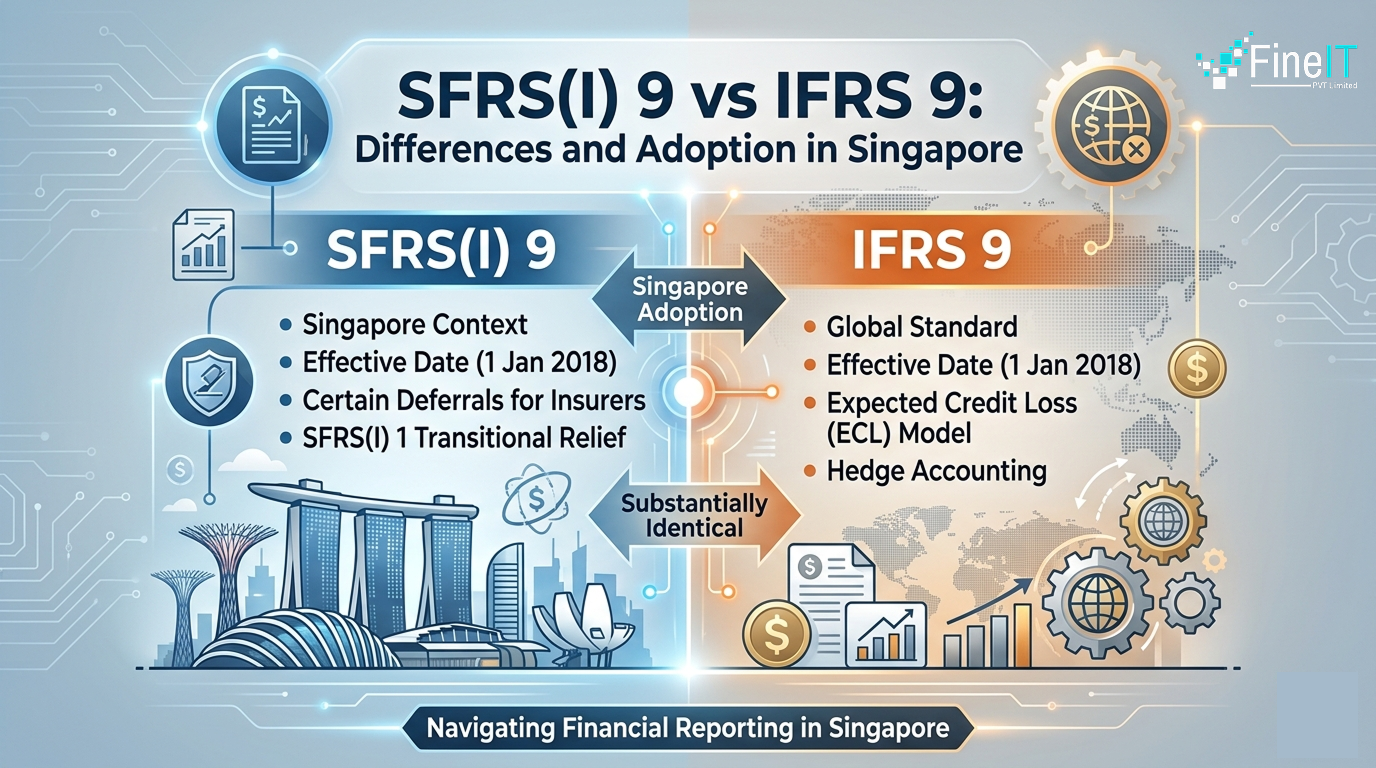

In the world of Singaporean finance, the shift to SFRS(I) 9 represented a landmark transition toward global transparency. While the names “SFRS(I) 9” and “IFRS 9” are often used interchangeably, understanding the specific context of Singapore’s adoption is crucial for businesses operating in the Lion City. As of 2026, Singapore remains fully committed to this […]