How the Monetary Authority of Singapore Supervises IFRS 9 Compliance

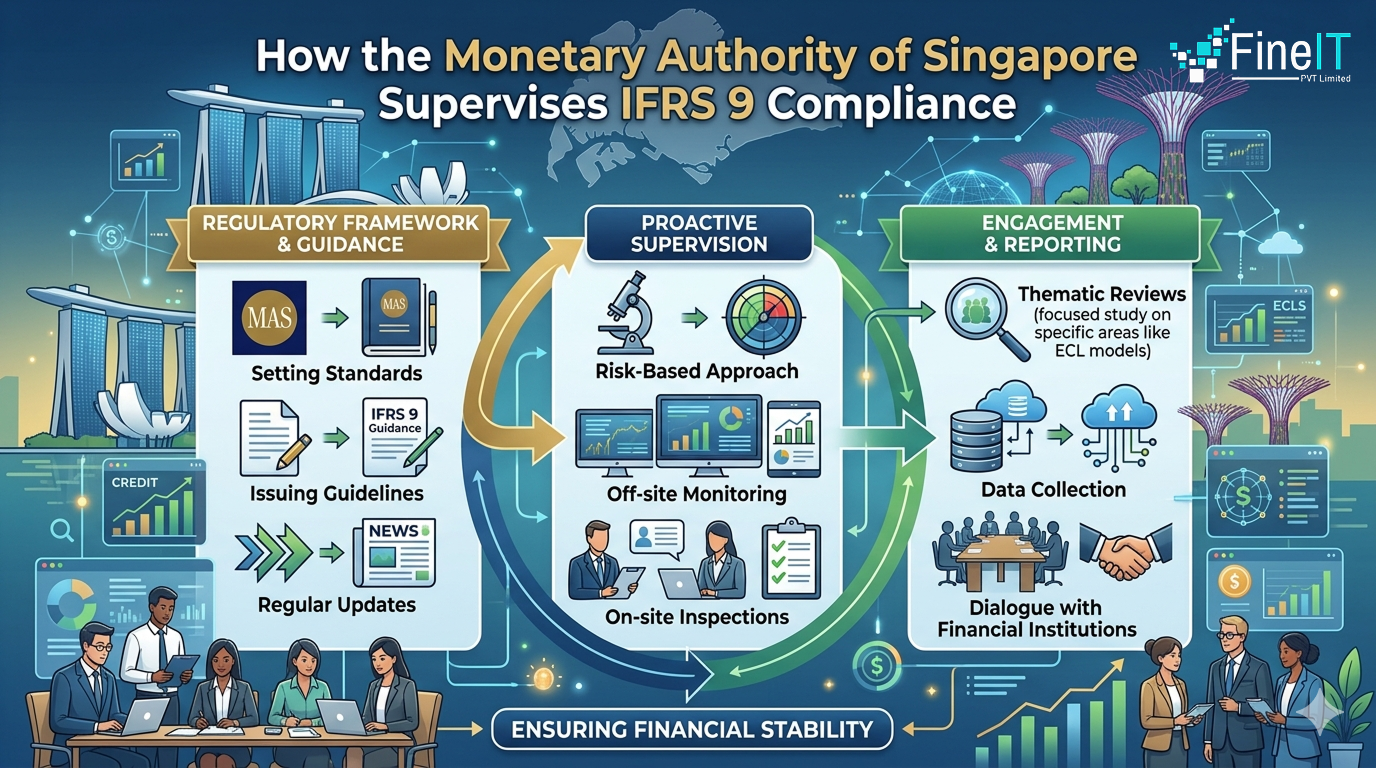

In the wake of the global shift toward more resilient accounting standards, the Monetary Authority of Singapore (MAS) has established itself as a rigorous overseer of IFRS 9 (SFRS(I) 9). This standard, which centers on the Expected Credit Loss (ECL) model, requires financial institutions to look into the future rather than the past. For MAS, […]