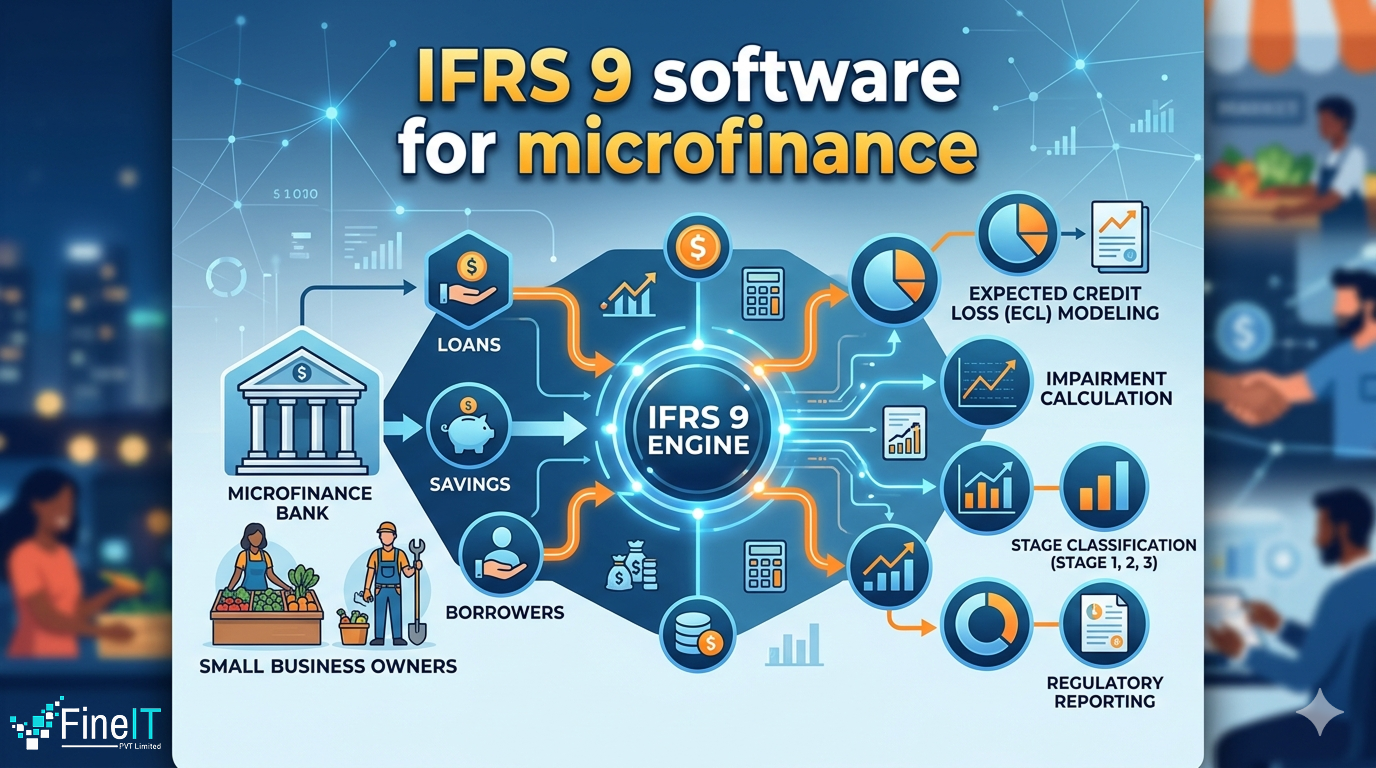

Beyond Compliance: Unlocking Value with IFRS 9

The implementation of IFRS 9 represents a fundamental shift in how financial health is assessed and managed. Rather than waiting for a default event to occur, the ECL framework requires institutions to incorporate past events, current conditions, and reasonable forecasts of future economic scenarios (Azhar, 2022). This structural change offers several avenues for value creation: […]