The transition to IFRS 9 (International Financial Reporting Standard 9) represents a paradigm shift in how financial institutions account for credit risk. For the microfinance sector—characterized by high-volume, low-value loans and borrowers often lacking traditional collateral—the stakes of this transition are uniquely high. Moving away from the old “incurred loss” model to the Expected Credit Loss (ECL) framework requires not just a change in accounting, but a complete overhaul of data management and risk strategy.

1. How has accounting shifted from incurred to expected credit losses?

Under the previous standard, IAS 39, losses were only recognized when an event (like a missed payment) had already occurred. IFRS 9 is forward-looking. It requires Microfinance Institutions (MFIs) to estimate future losses from the day a loan is issued.

How does the three-stage impairment model work?

The core of IFRS 9 is the staging of financial assets based on their credit quality:

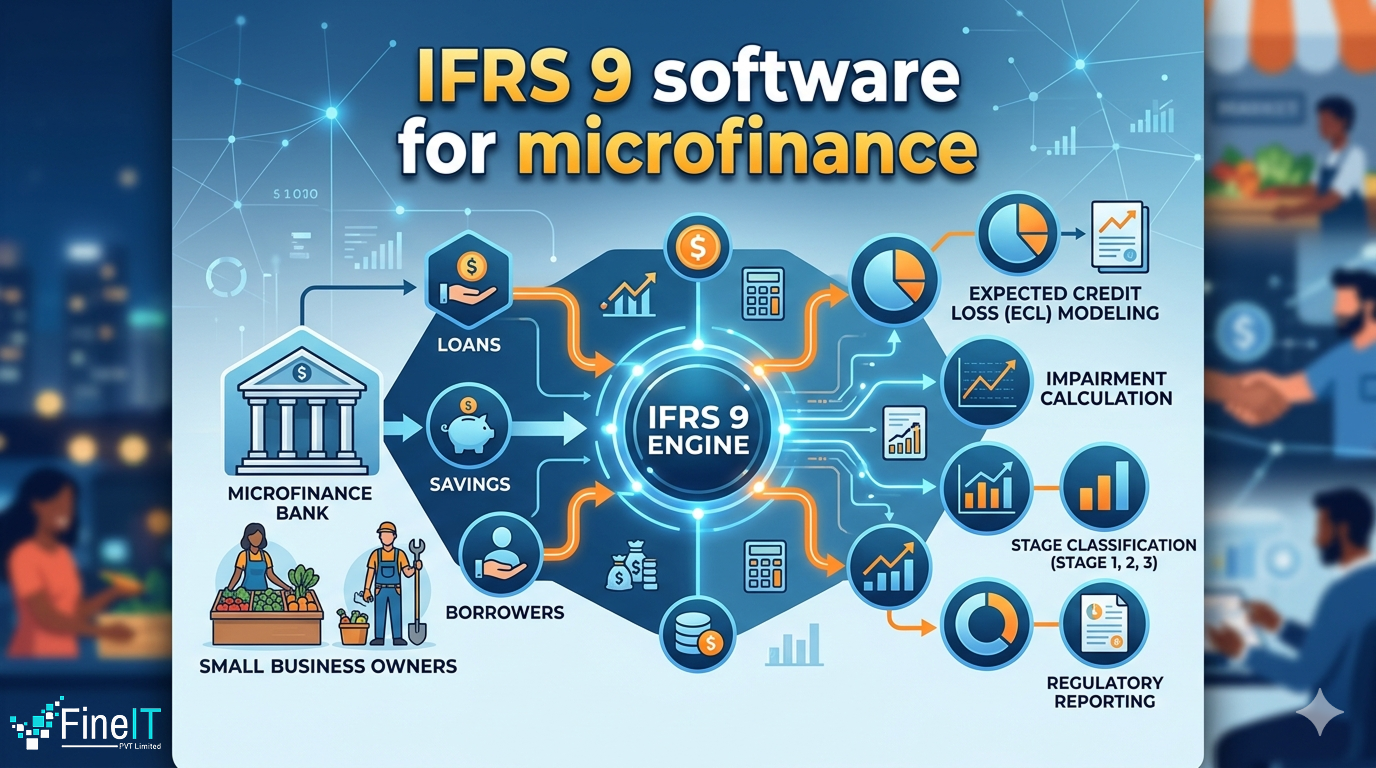

Stage 1 (Performing):

Loans that have not seen a significant increase in credit risk. MFIs must recognize 12-month ECL.

Stage 2 (Underperforming):

Loans where credit risk has increased significantly (SICR) since origination. These require Lifetime ECL provisions.

Stage 3 (Non-performing):

Loans that are credit-impaired or in default. These also require Lifetime ECL.

2. Why is specialized software essential for IFRS 9 compliance?

For many MFIs, the initial instinct is to manage IFRS 9 via complex Excel spreadsheets. However, the sheer volume of micro-loans and the complexity of the variables involved make manual processing a significant operational risk. Dedicated IFRS 9 software provides:

How does the ECL calculation engine function?

The software automates the most mathematically intensive part of the standard. The formula for Expected Credit Loss is generally expressed as:

$$ECL = PD \times LGD \times EAD$$

PD (Probability of Default):

The likelihood a borrower will fail to pay.

LGD (Loss Given Default):

The percentage of the exposure the MFI expects to lose if a default occurs.

EAD (Exposure at Default):

The total value the MFI is exposed to at the time of default.

B. Handling “Forward-Looking” Information

Microfinance is highly sensitive to macroeconomic shifts. Software allows MFIs to integrate external data—such as inflation rates, agricultural yields, or regional economic growth—into their risk models. If a drought is predicted, the software can automatically adjust the PD for rural portfolios, ensuring the MFI is adequately provisioned before the first payment is even missed.

3. What challenges arise when implementing IFRS 9 in microfinance?

While the benefits are clear, the path to implementation has unique hurdles:

Why are data quality and granularity important?

IFRS 9 requires historical data to build “Point-in-Time” models. Many MFIs struggle with fragmented data across legacy systems.

How do resource constraints impact IFRS 9 implementation?

Smaller MFIs may lack the internal actuarial or quantitative expertise to build and validate complex models.

How does earnings volatility affect IFRS 9 compliance?

Because provisions are now forward-looking, a sudden change in economic outlook can lead to a “spike” in provisions, impacting the institution’s reported profitability.

4. What key features should you look for in IFRS 9 software?

When selecting an IFRS 9 software solution, MFIs should prioritize:

What integration capabilities are necessary?

Does it connect directly to your Core Banking System (CBS)?

Why is scalability critical for IFRS 9 software?

Can it handle a portfolio growing from 10,000 to 100,000 borrowers?

What makes a user interface effective for IFRS 9 tools?

Is it accessible for finance teams, or does it require a PhD in statistics to operate?

How can software ensure audit readiness?

Can the software produce a “line-by-line” audit trail that shows exactly how a specific loan moved from Stage 1 to Stage 2?

What are the key takeaways for IFRS 9 implementation?

The implementation of IFRS 9 is more than a “check-the-box” regulatory exercise for microfinance institutions; it is a fundamental shift toward more sophisticated risk management. While the technical requirements—especially regarding Expected Credit Loss modeling—are rigorous, the adoption of specialized software transforms this challenge into a competitive advantage.

By utilizing automated solutions, MFIs can ensure regulatory compliance, provide greater transparency to investors, and, most importantly, gain a deeper understanding of their portfolio’s health. In the long run, the institutions that successfully navigate this transition will be more resilient, better capitalized, and better equipped to continue their mission of financial inclusion in an increasingly volatile global economy.

Partner with FineIT to transform your microfinance risk management—our AI-powered IFRS 9 solutions automate ECL modeling, enhance data accuracy, and deliver audit-ready insights at scale.

👉 Explore more: https://fineit.io/

👉 Book a demo: https://fineit.io/request-demo

Empower your institution with smarter compliance, faster decisions, and future-ready financial intelligence.

Frequently Asked Questions

About FineIT Private Limited

FineIT Private Limited is a leading Fintech provider.

Muzammal Rahim Khan is the CEO and Co-Founder of FineIT, bringing over 15 years of expertise in software development, implementation, and technical consulting across global markets including the U.S., U.K., Europe, Africa, and Asia. He has led the design and delivery of enterprise-grade solutions that modernize compliance, risk management, and financial reporting for banks and financial institutions. Under his leadership, FineIT has built flagship platforms such as Estimator9 (IFRS 9) and ContractHive (IFRS 16), empowering clients with automation, accuracy, and audit-ready confidence. Muzammal combines deep technical knowledge with strategic vision, driving innovation that bridges regulatory requirements with practical, scalable technology. His focus remains on building resilient, future-ready solutions that strengthen trust and efficiency in financial services.